Loyalty Program Liability: The Accounting Reality Most Founders Ignore

Most e-commerce founders treat loyalty points as a simple marketing cost—something to budget for and then forget about. The reality is far more complex and financially consequential. Every loyalty point you issue is a financial obligation that belongs on your balance sheet as a liability. This isn't accounting pedantry. Mismanaging loyalty program liability can distort your financial statements, trigger compliance issues, and erode investor confidence.

The myth is widespread because it's intuitive. You spend money issuing rewards, customers eventually redeem them, and that's that. But accounting standards like ASC 606 and IFRS 15 see it differently. They require you to defer revenue and recognize a liability the moment a customer earns points, not when they redeem them. The financial obligation exists whether the customer redeems next month or abandons the points entirely.

This distinction matters enormously. Getting it wrong means your financial statements misrepresent your true profitability and cash position. Getting it right builds credibility with investors, ensures regulatory compliance, and gives you the data needed to design your program strategically.

What Exactly Is Loyalty Program Liability?

loyalty points as store credit—a gift card your customer receives for free as part of their purchase. That's the essence of loyalty program liability.

When a customer buys $100 worth of products and earns 500 points (worth $10 in future rewards), your company has made a promise. You owe that customer $10 in value. From an accounting perspective, that promise is a debt. It sits on your balance sheet as a liability until one of three things happens: the customer redeems the points, the points expire, or they accumulate indefinitely.

The key insight: this liability exists immediately when points are earned, not later when they're redeemed. This is where accrual accounting comes in. Under accrual accounting (the standard for most businesses), you record expenses and revenues when they're incurred, not when cash changes hands. If you were running a cash-basis system (rare for retail), you'd only recognize the cost when the customer actually used their points. But accrual accounting, mandated by modern revenue recognition standards, treats it differently.

Under current standards like ASC 606 (used in the US) and IFRS 15 (the international equivalent), loyalty points represent what's called a "separate performance obligation." Here's what that means: when a customer makes a purchase, they're not just buying the product. They're also buying the right to future rewards. Those two things—the product and the future reward—are separate obligations.

So on day one, your company receives cash for the full $100 purchase. But you can't recognize all $100 as revenue immediately. A portion—typically calculated based on the standalone selling price of the loyalty points—gets deferred. That deferred amount becomes a liability on your balance sheet. It stays a liability until the customer either redeems those points (at which point you recognize the deferred revenue) or the points expire (at which point the liability shrinks based on your breakage assumption).

Consider this: if a concert venue sells a ticket with a free drink voucher for $50, they don't recognize all $50 as revenue on the day of sale. They defer a portion of that $50 until the customer either uses the drink voucher or it expires. Loyalty points work the same way.

Why Loyalty Program Liability Isn't Just "Nerd Stuff": Impact on Your Business

The accounting treatment of loyalty programs directly shapes how investors, lenders, and regulators perceive your financial health. Ignore it, and your balance sheet becomes unreliable.

Financial health starts with accuracy. When loyalty program liability is underreported or ignored entirely, your reported profits look artificially high. Your asset values appear overstated. A founder might look at their P&L and think the business is in stronger shape than it actually is. This becomes catastrophic when communicating with investors or preparing for fundraising. Sophisticated investors now scrutinize loyalty program accounting closely. They understand that outstanding points represent future cash outflow or revenue recognition adjustments. If your numbers don't account for this properly, they'll assume you're either unsophisticated about your finances or deliberately misrepresenting them. Neither perception helps your valuation.

Regulatory compliance is equally important. ASC 606 and IFRS 15 aren't suggestions—they're mandatory accounting standards. Public companies must comply. Private companies increasingly must comply as well, especially if they're seeking investment or planning an acquisition. Auditors will flag loyalty program liability accounting if it's not done correctly. You might be forced to restate financials, which damages credibility and can trigger regulatory inquiries. The cost of correction after the fact is far higher than doing it right from the beginning.

advanced loyalty for enterprises face additional scrutiny around compliance and investor relations. But the fundamental principle applies to all merchants: transparent, accurate financial reporting builds trust.

Strategic program design depends on understanding liability. If you don't know what your loyalty program actually costs your business in liability terms, you can't make informed decisions about earn rates, redemption values, or expiration policies. Should you double your earn rate? That increases liability dramatically. Should you offer never-expiring points? That pushes liability toward infinity (unless breakage is very high). Without this data, you're flying blind.

The Mechanics of Loyalty Program Accounting: Standards, Breakage, and Deferrals

The accounting framework governing loyalty programs emerged from a fundamental question: how should revenue be recognized when a company promises future goods or services? ASC 606 (issued by the Financial Accounting Standards Board) and IFRS 15 (the international equivalent) provide the answer using a five-step model.

Step one: identify the contract with the customer. In loyalty programs, the contract includes both the immediate product sale and the future reward obligation.

Step two: identify performance obligations within that contract. The product is one. The loyalty points are another.

Step three: determine the transaction price. This is what the customer pays—the $100 in our example.

Step four: allocate the transaction price to each performance obligation. This is where things get complex. You need to split that $100 between the product and the points based on their relative standalone selling prices.

Step five: recognize revenue as performance obligations are satisfied. The product revenue is recognized when shipped. The loyalty points revenue is deferred and recognized later (when redeemed or when they expire).

This model was implemented for US GAAP entities in 2018 and is now standard practice. It's not going away.

Within this framework, one variable dominates the accounting outcome: breakage rate. Breakage is the percentage of loyalty points expected to go unredeemed. If you estimate that 20% of issued points will never be redeemed, then only 80% of those points represent a true liability. The other 20% eventually becomes revenue when the points expire.

Why does breakage matter so much? Because it directly reduces reported liability and increases reported profits. A high breakage assumption means less deferred revenue, less balance sheet liability, and more recognized income. This creates a perverse incentive: companies might be tempted to over-estimate breakage to make their finances look better. But breakage estimation is a critical judgment area. Auditors scrutinize it closely. And if your actual redemption experience proves your breakage estimate wrong, you'll be restating financials later—far more damaging to credibility than accurate reporting now.

Estimating breakage requires data and discipline. Historical data is the foundation: what percentage of points have actually expired unredeemed in your program? But history isn't always a perfect guide. A new demographic joining your loyalty program might have different redemption behavior. A product line change might affect engagement. Program design changes (new rewards offered, higher point values, clearer expiration messaging) all shift breakage rates.

More sophisticated methods use statistical models. analyzing customer redemption patterns and behavioral data helps calibrate these models. Some companies now use machine learning to forecast breakage more accurately, accounting for customer segmentation, seasonality, and other variables.

Ready to increase customer lifetime value?

Join 100+ Shopify stores using Mage to turn one-time buyers into loyal repeat customers.

Alongside breakage, you need to determine the standalone selling price (SSP) of your loyalty points. This is the price at which you would sell the points separately if you actually did sell them (which most companies don't). Since points are rarely sold as standalone products, SSP must be estimated.

One method: adjusted market assessment. Look at how competitors price loyalty rewards and adjust for your specific program characteristics.

Another method: expected cost plus margin. Calculate the actual cost to fulfill a reward and add a reasonable profit margin.

A third method: residual approach. Take the total transaction price, subtract the standalone selling price of the product, and the remainder is the implied SSP of the points. This method works but is less transparent.

Once you have breakage rate and SSP, the math is straightforward. Liability = Outstanding Points × (1 – Breakage Rate) × SSP. This formula sits at the heart of loyalty program accounting and should be recalculated regularly as new data emerges.

The revenue recognition journey itself unfolds in stages. When points are earned, a portion of revenue is deferred and a liability is recorded. When points are redeemed, that liability shrinks and the deferred revenue is recognized. When points expire, the remaining liability for those points is eliminated, and the corresponding amount flows to the income statement as "breakage revenue" or "revenue from expired points."

Applying the Principles: Managing & Reporting Your Loyalty Liability

The formula is simple. Application is where precision matters.

Let's use a concrete example. Assume:

- A customer makes a $100 purchase

- Your system allocates 5% of the transaction price ($5) to loyalty points

- You estimate a 20% breakage rate

- The SSP of loyalty points is $1 per 100 points earned

The calculation:

- Deferred revenue = $5 × (1 – 0.20) = $4 deferred

- Revenue recognized immediately on the sale = $96

- Liability recorded = $4

Later, if the customer redeems those points for a $5 reward, the $4 liability is eliminated and $4 of revenue is recognized. If the points expire unredeemed, the $4 liability is reversed and $4 flows to breakage revenue.

Across thousands or millions of transactions, this compounds into a significant balance sheet item.

Effective accruals management for e-commerce requires several components working together. First, your loyalty platform must accurately track every point issued. This seems obvious but many systems have gaps. Points issued through promotions, bonus programs, or referrals sometimes get recorded differently than purchase-based points. Standardization is critical.

Second, you need regular reassessment of key assumptions. Breakage rates should be reviewed at least annually, or whenever significant program changes occur. If you increase your earn rate, lower redemption thresholds, or expand reward options, customer behavior shifts. Your breakage assumption needs to move with it.

Third, understanding redemption patterns gives you insight into program health. When do customers redeem? What types of rewards are most popular? Do certain customer segments show higher or lower redemption rates? These insights help refine both your breakage estimates and your program design.

Fourth, your loyalty platform must integrate cleanly with your accounting system. Manual data exports and spreadsheet entry create errors. Automation reduces friction and improves accuracy. Platforms such as Mage Loyalty, Rivo, and Growave increasingly offer export features designed to feed directly into accounting workflows.

choosing the right loyalty platform becomes strategic when you factor in accounting requirements. You need a platform that can provide the data your accountants need in the format they need it.

loyalty program expiration policies directly affect liability. Points that never expire create indefinite liabilities unless your breakage rate is extremely high. Points with short expiration windows reduce liability faster (higher breakage) but may frustrate customers. The design choice has both financial and customer experience consequences.

Practically speaking, your journal entries will look like this:

When points are issued (at time of sale):

Debit: Loyalty Program Expense (or Deferred Revenue)

Credit: Loyalty Program Liability

This entry records the obligation created by points issued.

When points are redeemed:

Debit: Loyalty Program Liability Credit: Revenue (or Cost of Goods Sold, depending on how you structure it)

This entry recognizes that the obligation has been fulfilled.

When points expire unredeemed:

Debit: Loyalty Program Liability Credit: Breakage Income

This entry recognizes the portion of the obligation you'll never have to fulfill.

For investors and auditors, financial statement disclosures matter. You must disclose your accounting policy for loyalty programs. You must explain how you estimate SSP and breakage rates. You must provide a reconciliation (roll-forward) of the contract liability balance, showing opening balance, points issued, points redeemed, and points expired. You should disclose the expected settlement period for outstanding obligations (e.g., "approximately 60% of outstanding points are expected to be redeemed within 12 months").

These disclosures build transparency. They show investors that you understand your business and can accurately represent its financial position.

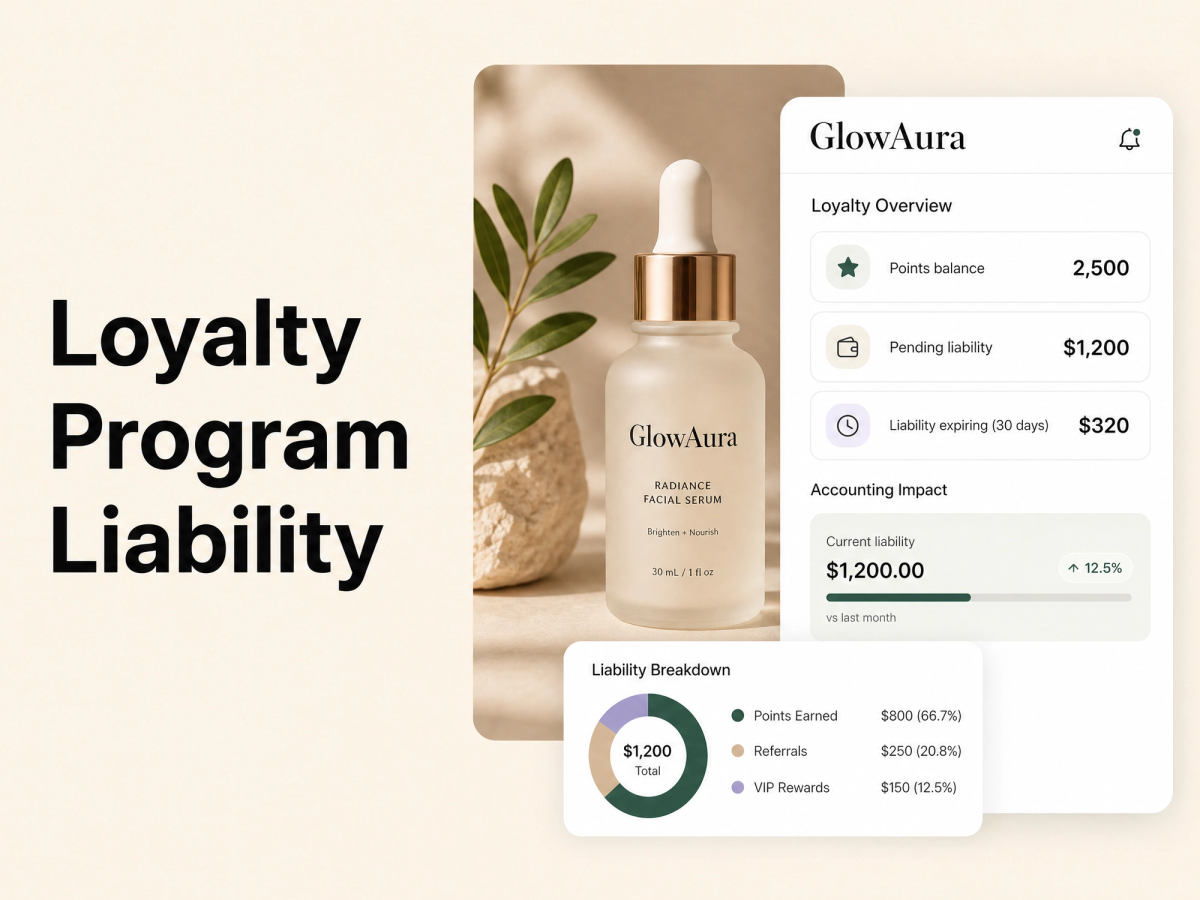

Mage's Solution: Exportable Liability Reports for E-commerce Founders

E-commerce founders operate in a unique environment. Your loyalty program is likely integrated with your Shopify store, connected to your email platform and POS system if you have one, and generating transaction data constantly. Yet most off-the-shelf accounting software doesn't speak Shopify natively, and most loyalty platforms don't export data in accounting-friendly formats.

This gap creates friction. Founders resort to manual exports and spreadsheet calculations, introducing error risk and consuming time better spent on strategy.

Mage Loyalty's exportable liability reports address this gap directly. The feature aggregates real-time data on outstanding points, their estimated cost per redemption, and the resulting balance sheet liability. The reports are formatted to be immediately useful to your accounting team or external accountant. No translation layer required.

What these reports provide:

Real-time aggregation of outstanding points across your loyalty program, segmented by expiration date, earn type (purchase, referral, bonus), and customer segment if desired.

Estimated liability using your configured breakage rate and cost-per-point assumptions. Updates as program parameters change, so you always have current numbers.

Detailed breakage assumptions used in the calculation, documented for audit purposes and investor transparency.

Valuation methodologies explained, so your accountant understands exactly how the numbers were derived.

Export in formats (CSV, PDF, Excel) that integrate cleanly into accounting workflows.

For merchants, this automation solves several problems simultaneously. Accuracy improves because there's no manual data reentry. Compliance becomes easier because the data aligns with accounting standards. Decision-making improves because founders can model "what-if" scenarios (what if we increase the earn rate? What happens to liability?) in real time.

Most importantly, it shifts loyalty program accounting from a burden to a strategic tool. Instead of scrambling to collect data for auditors or investors, you have it ready.

Frequently Asked Questions

Is loyalty program liability something only large companies need to worry about?

No. ASC 606 and IFRS 15 apply to all entities recognizing revenue from contracts with customers, regardless of size, if loyalty points are a material commitment. "Material" is a judgment call, but any meaningful loyalty program should be accounted for properly. Smaller companies sometimes get more flexibility in how they document assumptions, but the principles are the same. A Shopify store with a growing loyalty program should be thinking about this now, not later when complexity becomes unmanageable.

How often should I recalculate my breakage rate?

At minimum, annually. More frequently if your program changes significantly (new reward types, different earn rates, modified expiration policies, expanded customer base into new demographics). Some companies recalculate quarterly if they're operating in a dynamic environment. The key is having a documented, systematic approach. Auditors will ask how often you review this assumption and why.

What if my loyalty points never expire?

This is a complicated scenario. Never-expiring points create indefinite liabilities. Unless your historical breakage is extremely high (customers actively choose not to redeem), the liability stays on your balance sheet indefinitely. This creates a drag on reported profitability and can concern investors. Many programs moved to expiration policies specifically because of the accounting implications. If you're considering a never-expire model, factor the balance sheet impact into your decision.

Can better program design actually reduce liability?

Yes. Expiration policies reduce it. Encouraging faster redemption reduces it. Making redemption more attractive and frictionless increases redemption rates, which reduces breakage, which reduces liability. From a strategic standpoint, there's often a win-win: program design that maximizes customer satisfaction and engagement also manages balance sheet liability more efficiently.