Points vs Cashback vs Store Credit: Which Reward Model Wins on Shopify?

# Points vs Cashback vs Store Credit: Which Reward Model Wins on Shopify?

Here's a truth that surprises most Shopify merchants: traditional loyalty points aren't actually your golden ticket to retention. In fact, they underperform dramatically. The industry average redemption rate for points-based programs sits around 18%, while modern store credit systems achieve 40% or higher. Yet most merchants still default to points, assuming they'll create the "most impressive" customer experience. This assumption costs businesses millions in unredeemed value every year.

The loyalty landscape has fundamentally shifted. What worked five years ago—flashy points with complex conversion ratios—no longer dominates. Today's winners balance earning mechanisms that engage customers with redemption pathways that actually get used. Understanding which model fits your specific business is no longer optional. It's the difference between a loyalty program that drives 12-18% annual revenue growth and one that quietly sits dormant.

This guide unpacks the three dominant reward models, reveals which performs best for different customer profiles and average order values, and introduces a hybrid approach that combines the psychological appeal of points with the redemption power of store credit.

Understanding the Three Loyalty Models: A Foundation

Think of these three models as different currencies in a global payment system. Each one solves a different customer need and creates distinct merchant incentives. They're not interchangeable, and choosing wrong can undermine your entire retention strategy.

Loyalty Points: The Proprietary Currency

Loyalty points are a virtual currency created and controlled entirely by your brand. When customers purchase, refer friends, write reviews, or hit birthdays, they accumulate points in their account. Those points can eventually be redeemed for merchandise, discounts, gift cards, or store credit—depending on your rules.

The psychological appeal is real. "You've earned 5,000 points!" sounds more generous than "You've earned $5 off." This perception of abundance drives engagement. Points also create flexibility. You can reward dozens of different behaviors without discounting prices, and you control the conversion ratio (maybe 100 points equals $10, or 200 points equals a free product). This customization is powerful.

But here's where points falter: complexity kills redemption. When customers don't understand the true value of their points, or when redemption requires friction (hunting for eligible products, minimum purchase thresholds), redemption rates crater.

Cashback: Real Money, Real Simplicity

Cashback is straightforward. Customers earn real currency—actual dollars or credits—that they can withdraw to a bank account, e-wallet, or credit card. Unlike points, cashback has no mystery. $5 earned equals $5 value, spendable anywhere.

Cashback programs typically fund rewards through affiliate budgets, meaning the merchant isn't reducing margins at checkout. This structure protects profitability while still rewarding customers generously. Cashback also stacks with other promotions and credit card rewards, adding genuine value without creating confusion.

The catch? Cashback is flexible in all directions. Customers can take their rewards anywhere, which means less money stays within your store. For merchants focused on customer lifetime value and repeat purchases within their ecosystem, this open-ended flexibility can dilute loyalty.

Store Credit: Money That Stays

Store credit is an amount deposited into a customer's account that's usable only at your store, on future purchases. It can be issued for returns, purchases, sign-ups, referrals, birthdays—any action you want to reward. The beauty lies in control.

You decide when it expires (or if it expires), which products it covers, and minimum spend requirements. Once a customer has store credit, they psychologically own it. Loss aversion kicks in—they don't want to "waste" that money, so they're more likely to return and spend. This endowment effect is powerful. The credit feels like their money now, not a brand's generosity.

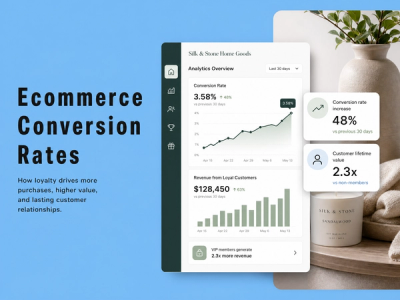

Modern platforms leveraging Shopify's native store credit system have transformed this model. They've eliminated the friction points that made store credit feel restrictive. The result? Shopify's native store credit system achieves redemption rates that would astound merchants using traditional points. We're talking 40%+ versus 18%.

Why This Matters: The Business Impact of Redemption

Here's where theory meets profit. Almost 75% of business revenue comes from retained customers. Loyalty programs can drive 12-18% annual revenue growth through repeat purchases alone. But only if customers actually redeem rewards.

An unredeemed reward is a phantom liability on your books and a missed opportunity to drive repeat purchases. Worse, it creates customer dissatisfaction. Customers earn rewards but never use them. They feel cheated. They leave.

The redemption problem isn't just about numbers. It's about retention psychology. When a customer actually redeems a reward, they've committed to a repeat purchase. They've used your store again. They've updated their mental framework of your brand from "place I bought once" to "place I buy from." That shift is permanent.

Beyond retention, different models impact your bottom line differently. Cashback programs can reward full-price purchases, protecting margins better than blanket discounts. Store credit keeps customer lifetime value concentrated within your brand ecosystem. Points create flexibility to reward non-monetary behaviors like referrals and reviews, building community alongside transactions.

Ready to increase customer lifetime value?

Join 100+ Shopify stores using Mage to turn one-time buyers into loyal repeat customers.

Head-to-Head Comparison: What the Data Shows

Let's move past theory and look at what actually happens on Shopify stores running each model.

Redemption Rates: The Defining Metric

The single most important performance indicator for any loyalty program is redemption rate. A program with zero redemptions generates zero impact.

Modern store credit systems consistently outperform traditional points. This isn't random. The reason is behavioral. Store credit feels like customer funds. Points feel like brand currency. When it's your money, you use it. When it's their currency, with unclear value, you often don't.

Loyalty members spend 164% more when redeeming rewards compared to non-members across all program types. But this only matters if redemptions happen. Historical data shows that traditional points programs average 18% redemption rates. Modern store credit systems achieve 40%+ redemption rates—more than double.

Programs like Rivo's can lead to 3.1x repeat purchase rate improvements and deliver 52x ROI for Shopify Plus brands. These numbers come from hybrid and store credit models, not pure points.

Comparison Table: Points vs. Cashback vs. Store Credit

| Dimension | Points | Cashback | Store Credit |

|---|---|---|---|

| Definition | Proprietary brand currency earned through actions | Real money earned and withdrawable anywhere | Store-specific balance usable for future purchases |

| Reward Type | Virtual, needs redemption | Real currency | Store-specific currency |

| Flexibility of Use | Limited to your store | Unlimited, spendable anywhere | Your store only |

| Ease of Understanding | Moderate (conversion ratios can confuse) | High (direct value) | High (clear balance) |

| Average Redemption Rate | 18% (industry standard) | Varies by platform | 40%+ (modern systems) |

| Merchant Control | High (control all mechanics) | Moderate (limited by real money) | Very High (expiry, categories, minimums) |

| Margin Impact | Flexible, can protect margins | Impacts margins more directly | Keeps funds internal, high control |

| Best For | Engagement, gamification, multi-behavior rewards | Transparency, customer simplicity | Retention, AOV, keeping value internal |

Matching Models to Your Business Profile

Not every model works for every Shopify store. The fit depends on three factors: average order value, purchase frequency, and your customer's primary motivation.

Low AOV, High Frequency (Consumables, Subscriptions)

Examples: coffee subscriptions, beauty consumables, snacks.

These customers buy frequently but in small amounts. They value speed and immediate gratification. They don't want to accumulate points over months for a meaningful reward.

Best model: Cashback or simple, easily redeemable points with low thresholds.

Why: Frequent buyers see immediate value. A 5% cashback on a $15 purchase yields $0.75 they can use instantly or accumulate quickly. Points programs work here too, but only if redemption thresholds are extremely low—think 25 points per $1 spent with rewards starting at 25 points for a $5 discount.

Mid AOV, Moderate Frequency (Fashion, Lifestyle, Home Goods)

Examples: Kitsch (hair and beauty), apparel brands, home decor.

These customers have brand loyalty potential. They don't buy constantly, but when they do, they're willing to spend $50-200+. They respond to recognition and want to feel part of a community.

Best model: Store credit or hybrid points+credit models.

Why: Store credit incentivizes return visits. Once a customer has $20 in store credit, they're psychologically motivated to return and spend more. Kitsch generated $5.8M in loyalty-attributed revenue with 1.2M activated customers using a Rivo-powered program—precisely this model. A hybrid approach lets customers earn points through various behaviors (referrals, reviews, purchases) while converting those points to store credit, which drives redemptions.

High AOV, Considered Purchases (Luxury, Premium Electronics)

Examples: HexClad cookware, designer goods, electronics.

Customers here make infrequent, deliberate purchases. They're investing in quality. They respond to significant rewards that feel worthy of their investment.

Best model: Value-driven points (for aspirational rewards) or cashback (for substantial savings).

Why: A customer spending $400 on a premium pan deserves a reward that feels proportional. Points programs with tiered redemptions work well here—earn points that accumulate toward exclusive experiences, premium products, or significant discounts. HexClad achieved 92x ROI and $450,000 in referral revenue through a points-based referral program, precisely because the reward matched the customer's investment level.

Customer Segmentation: The Psychographic Angle

AOV and frequency matter, but so does psychology. Different customer types respond to different reward structures.

The Bargain Hunter

Motivated by: Direct savings, value, price consciousness.

Best model: Cashback. They want tangible, transparent value. Points with unclear conversion ratios frustrate them. Cashback delivers immediate, quantifiable benefit.

The Brand Loyalist

Motivated by: Recognition, exclusivity, deeper relationship with the brand.

Best model: Store credit or points with VIP tiers. These customers want to feel special. They're already committed to your brand. Reward that commitment with recognition, exclusive access, or tiered benefits that make them feel valued.

The Gamified Shopper

Motivated by: Progress tracking, achievements, leaderboards, unlocking status.

Best model: Points with tiered levels, badges, or milestone rewards. These customers want to see progress. A dashboard showing their point accumulation, tier progress, and upcoming rewards is engaging. Gamification drives behavioral psychology—the desire to level up is real.

The Real Cost: What Each Model Demands

Merchants often underestimate the costs associated with each program.

Points Programs

Financial liability: Outstanding unredeemed points represent a contingent liability on your balance sheet. If you've issued 1 million points valued at $0.01 each and only 18% redeem, you're carrying $8,200 in dead liability.

Operational costs: Moderate. You need platform infrastructure, customer communication about earning/redemption mechanics, ongoing management of point balancing.

Margin impact: Low to moderate. You control the cost of points because they're your currency. But if redemption rates are low, you're spending money to maintain a program with minimal impact.

Cashback Programs

Financial liability: Lower. Cashback is real money, so you account for it as you pay it out.

Operational costs: Moderate to high. Affiliate commissions, payment processing fees, potential fraud management.

Margin impact: Direct and measurable. Every dollar of cashback comes directly from your margin. A 5% cashback program on $100,000 in monthly sales costs you $5,000.

Store Credit Programs

Financial liability: Medium. Issued store credit is a liability until spent. But spending rates are high (40%+), so this resolves quickly.

Operational costs: Low to moderate. Modern platforms automate issuance and tracking. Less manual management than points.

Margin impact: Flexible and controllable. Store credit doesn't leave your ecosystem. When a customer redeems $20 in store credit, they typically spend additional funds. If your margin is 40%, that $20 redemption might generate $8 in margin while also driving a repeat purchase.

Introducing the Hybrid Model: Points + Store Credit

The most sophisticated Shopify brands don't choose a single model. They combine them.

A hybrid approach layers points for earning and engagement with store credit for redemption and retention. Here's how it works:

Customers earn points through multiple behaviors: purchases (1 point per $1), referrals (50 bonus points), reviews (25 points), birthday sign-ups (10 points). This engagement mechanism is what makes points valuable. It lets you reward non-monetary actions.

Those points then convert to store credit (say, 100 points = $10 store credit) or customers receive store credit directly for specific actions. This redemption mechanism is what makes the program sticky. Store credit drives return visits and boasts 40%+ redemption rates.

Mage Loyalty's innovative hybrid approach combines flexible point earning with strong store credit redemption mechanics. Merchants can customize point earning rules for any behavior, then define how those points convert to store credit. It's the engaging earning mechanism of points paired with the redemption power of store credit.

Why does this work? It addresses both psychological drivers. The earning phase satisfies the need for engagement and recognition. The redemption phase satisfies the need for tangible value. Customers see progress (points accumulating) and experience gratification (store credit they can use immediately).

Making Your Choice: A Practical Framework

Start by answering three questions:

First: What's your primary retention goal? Are you trying to increase purchase frequency (store credit)? Drive transaction value (cashback rewards on full-price items)? Build community through engagement (points for reviews and referrals)?

Second: What's your customer's psychology? Do they want simplicity and transparency (cashback)? Recognition and status (points with tiers)? Or a balance of both (hybrid)?

Third: What's your technical capacity? All three models are well-supported on Shopify through platforms like Mage Loyalty, Rivo, Growave, Smile.io, and LoyaltyLion. But setup complexity varies. Hybrid models require more sophisticated platform capabilities.

Seamless Integration: The Implementation Reality

Choosing a model means nothing if it doesn't integrate smoothly with your existing stack.

Modern Shopify loyalty platforms handle the heavy lifting. They connect to your store's native payment systems, integrate with email platforms like Klaviyo for automated communications, and sync customer data across touchpoints. This integration matters enormously.

A loyalty program siloed from your email marketing platform is a loyalty program customers forget about. One that integrates with Klaviyo means a customer who earns points receives an automated email celebrating their progress. A customer with available rewards receives a reminder. A customer who redeems gets recognition. These touchpoints compound behavior.

For omnichannel brands with Shopify POS, integration extends in-store experiences. A customer who earns points online can redeem them in-store, and vice versa. This consistency builds trust and increases lifetime value.

Fraud Prevention: The Hidden Necessity

Particularly with referral-heavy loyalty programs, fraud prevention becomes critical.

Bad actors will exploit loyalty programs. They'll create fake accounts to generate referral bonuses, use bots to post reviews for points, or manipulate tier systems. Protect against loyalty program abuse through verification systems.

Platforms should include verification mechanisms—requiring email confirmation for referrals, reviewing suspicious referral patterns, flagging automated review submissions. Some programs require social proof (following your brand on social media) to unlock certain rewards. This deters casual fraud.

Measuring What Matters: Key Metrics

Once your program launches, track these metrics obsessively:

Engagement metrics: Enrollment rate (what % of customers join), active participation (how many members are earning rewards regularly), action diversity (are customers earning through multiple channels, or only purchases?).

Redemption metrics: Redemption rate (what % of issued rewards get redeemed), average redemption value (how much does a customer typically redeem at once), time to redemption (how long between earning and redeeming).

Business impact: Customer lifetime value (compare members vs. non-members), repeat purchase rate (how often do members return), AOV impact (do members spend more per transaction), and revenue attribution (how much revenue came from loyalty-attributed purchases).

Quality metrics: Customer satisfaction (NPS or CSAT among program members), retention lift (do members stick around longer?), and referral performance (if applicable).

The most important single metric is redemption rate. A program with high engagement but low redemption is broken. A program with lower engagement but high redemption is working. You want both, but redemption is non-negotiable.

Real-World Examples: What Succeeds

Kitsch: Store Credit Excellence

Kitsch, a hair and beauty brand, deployed a loyalty program emphasizing store credit and rewards. They activated 1.2M customers and generated $5.8M in loyalty-attributed revenue. This result came from a program structure that rewards purchases with points that convert to store credit, driving repeat visits.

HexClad: Referral-Driven Points

HexClad, the premium cookware brand, emphasized referrals within a points program. They achieved 92x ROI and generated $450,000 in referral revenue. Their customer psychology is clear: premium cookware buyers are willing to refer because they're enthusiastic about the product. Reward that enthusiasm with points, and conversion follows.

SkinnyMe Tea: Tiered Gamification

SkinnyMe Tea combines points earning with VIP tier progression. Customers see clear milestones (reach Gold tier for free shipping). This gamification maintains engagement and drives repeat purchases as customers chase the next tier unlock.

Your Next Steps

Choosing the right loyalty model isn't about finding the objectively best option. It's about alignment. Align the model with your customer psychology, your AOV, your retention goals, and your operational capacity.

If you operate a low-AOV, high-frequency business and want simplicity, cashback wins. If you're mid-AOV and want maximum retention within your ecosystem, store credit wins. If you want engagement flexibility with strong redemption, a hybrid model wins.

Explore Mage Loyalty's hybrid solution for a balanced approach combining points earning flexibility with store credit redemption power. Or evaluate other Shopify-native platforms like Rivo, Growave, and Smile.io.

The cost of not choosing is higher than the cost of choosing imperfectly. Loyalty programs that drive 12-18% annual revenue growth don't appear by accident. They're built intentionally, measured rigorously, and optimized continuously.

Frequently Asked Questions

What is the average redemption rate for loyalty points programs?

The average redemption rate for traditional loyalty points programs sits around 18%, significantly lower than modern store credit systems which achieve 40% or higher. Redemption rates are the defining metric for program success because unredeemed rewards drive no repeat purchases and create customer dissatisfaction.

Can I run multiple reward models on my Shopify store simultaneously?

Yes, many Shopify stores successfully combine points, cashback, and store credit within a single hybrid program. For example, a store might offer 1 point per $1 spent (points earning) with those points converting to store credit (redemption), while also offering referral bonuses in store credit. Platforms like Mage Loyalty, Rivo, Growave, and Smile.io support flexible hybrid configurations.

How do loyalty programs impact customer retention?

Loyalty program members spend 164% more when redeeming rewards compared to non-members. More broadly, retention-focused programs drive 12-18% annual revenue growth from repeat purchases alone. Members return more frequently, have higher lifetime value, and are more likely to refer friends. The impact scales dramatically when redemption rates are optimized.

What's the difference between store credit and a discount code?

Store credit is issued directly to a customer's loyalty account and reflects balance they can see and spend over time. Discount codes are one-time offers sent via email or promotions. Store credit drives stronger retention because customers feel they "own" the balance and are motivated by loss aversion to return and spend it. Store credit also creates better tracking and enables tiered, personalized issuance based on behavior.

Is store credit only useful for returns?

No. While store credit can be issued for returns, modern loyalty programs issue store credit for any desired behavior: purchases, referrals, reviews, sign-ups, birthdays, or achieving VIP tier status. This flexibility lets merchants customize when and how store credit is earned, driving specific behaviors while maintaining the high redemption benefits store credit provides.

Which loyalty model works best for fashion brands?

Fashion brands typically succeed with store credit or hybrid points+credit models. Fashion customers have strong brand loyalty potential and don't buy constantly, making repeat visit incentives (store credit) more valuable than instant cashback. Mid-to-high AOV also supports tiered models that reward top spenders with exclusive benefits. Brands like Kitsch have generated $5.8M in loyalty-attributed revenue using store credit-focused models.

TLDR

No single loyalty model dominates—the winner depends on your AOV, purchase frequency, and customer psychology. However, data reveals a critical myth: traditional points programs underperform dramatically, averaging only 18% redemption rates versus 40%+ for modern store credit systems. Low-AOV, high-frequency businesses thrive with cashback. Mid-AOV, repeat-purchase brands win with store credit. High-AOV, considered purchases respond to valuable points. For most Shopify brands, a hybrid points+credit model balances earning engagement with redemption power, driving 12-18% annual revenue growth from repeat purchases while keeping customer value concentrated within your store.